Written by

Written by

Edited by

Edited by

Optimum First Mortgage 30 Year Fixed

NMLS #240415 | State Lic: RM.804405.000

- RateRate as of 8/8/26

- 5.623%

- APRAPR

- 5.858%

- Monthly paymentMonthly payment

- $2,026

- Points

- 1.965

- Upfront costs

- $8,912

- 8-year cost

- $157,890

- Customer score

Real time rates for Aug 08, 2026

Select a mortgage type to compare national averages with top offers on Bankrate.

APRs not included. For our most recent APR information, please visit our rate table

The average rate for 30-year, fixed-rate home loans fell to 6.63% this week, according to Bankrate's national survey of lenders. That was down from 6.67% the previous week.

Despite the small drop in rates, mortgage rates are still near their highest levels in a year. And that’s discouraging Americans from buying homes or refinancing their home loans.

“Application volume for both refinance and purchase loans declined for the week, and [both] are now running behind last year’s pace, indicating that higher mortgage rates have weakened overall demand,” Mike Fratantoni, chief economist of the Mortgage Bankers Association, said Aug. 5.

Last week’s major economic headline came from the Federal Reserve, which kept its benchmark rate unchanged — though experts think the central bank may raise it at the September meeting. This week’s big news comes Aug. 7, when the Bureau of Labor Statistics releases its July jobs report. And next week brings the monthly inflation report, also from the BLS.

While mortgage rates aren’t set by the Fed, they have been pushed higher by the same forces that have kept the central bank from lowering its benchmark interest rate: inflation and unrest in the Middle East. Inflation slowed to an annual pace of 3.5% in June — down from 4.2% in May, according to the Labor Department — but it’s still well above the Fed’s 2% target. Inflation has been pushed up by oil prices, which briefly topped $100 a barrel as the U.S.-Iran war resumed, although they’ve come down in recent days.

Should the latest headlines cause you to pump the brakes on your homebuying plans? Probably not. You’ll own your home for years, while mortgage rates bounce around by the hour.

But in this moment of elevated rate rates, it’s more important than ever to shop around for a mortgage. Bankrate research finds that 87% of Americans overpay for their home loans because they settle for the first offer they get. For the typical borrower, that adds up to $3,343 in extra costs each year.

Every year, American homeowners pay an average of $3,656 more than they need to. Compare rates today to get your best available rate and avoid overpaying.

Showing results for: Single-family home, 30 year fixed mortgages with all points options.

For live offers, represented by the solid button on each, we earn a fixed fee if you connect with the lender.

Showing 7 of 7

About our Mortgage Rate Tables: The above mortgage loan information is provided to, or obtained by, Bankrate. Some lenders provide their mortgage loan terms to Bankrate for advertising purposes and Bankrate receives compensation from those advertisers (our “Advertisers”). Other lenders' terms are gathered by Bankrate through its own research of available mortgage loan terms and that information is displayed in our rate table for applicable criteria. In the above table, an Advertiser listing can be identified and distinguished from other listings because it includes a “Next” button that can be used to click-through to the Advertiser's own website or a phone number for the Advertiser.

Availability of Advertised Terms: Each Advertiser is responsible for the accuracy and availability of its own advertised terms. Bankrate cannot guaranty the accuracy or availability of any loan term shown above. However, Bankrate attempts to verify the accuracy and availability of the advertised terms through its quality assurance process and requires Advertisers to agree to our Terms and Conditions and to adhere to our Quality Control Program. Click here for rate criteria by loan product.

Loan Terms for Bankrate.com Customers: Advertisers may have different loan terms on their own website from those advertised through Bankrate.com. To receive the Bankrate.com rate, you must identify yourself to the Advertiser as a Bankrate.com customer. This will typically be done by phone so you should look for the Advertisers phone number when you click-through to their website. In addition, credit unions may require membership.

Loans Above $832,750 May Have Different Loan Terms: If you are seeking a loan for more than $832,750, lenders in certain locations may be able to provide terms that are different from those shown in the table above. You should confirm your terms with the lender for your requested loan amount.

Taxes and Insurance Excluded from Loan Terms: The loan terms (APR and Payment examples) shown above do not include amounts for taxes or insurance premiums. Your monthly payment amount will be greater if taxes and insurance premiums are included.

Consumer Satisfaction: If you have used Bankrate.com and have not received the advertised loan terms or otherwise been dissatisfied with your experience with any Advertiser, we want to hear from you. Please click here to provide your comments to Bankrate Quality Control.

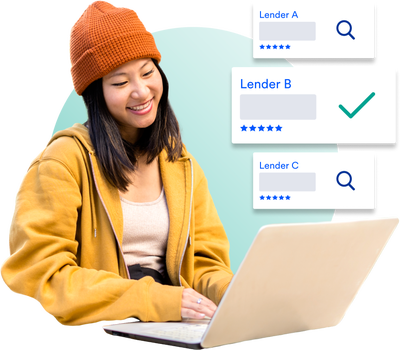

Most lenders show one rate: theirs. We show offers from multiple lenders competing for your loan, so you can compare and find a better one.

Answer a few quick questions so lenders can show rates tailored to you, not generic numbers.

See your top offers and choose which lenders to hear from — only those lenders will contact you.

We appreciate your feedback

Thank you for taking the time to share your experience.