Forecast survey: Fed seen as keeping rates at rock bottom through yield-curve control

The Federal Reserve is seen as increasingly likely to keep interest rates at near-zero percent until 2023 or beyond and will find new ways to keep borrowing costs at rock-bottom levels.

That’s according to a growing number of financial and economic experts surveyed for Bankrate’s June Fed Forecast poll, which found that more than a third (or 34 percent) say the U.S. central bank won’t be able to lift rates for three to four years. Just 29 percent of experts said this during the prior survey period in April.

But fighting off a downturn that Fed Chairman Jerome Powell has equated as the worst economic crisis in generations is only half the battle. The Fed will turn to new tactics similar to quantitative easing (Q.E.) that include capping yields on certain Treasury securities and expanding its balance sheet to unprecedented levels. The U.S. central bank is unlikely to cut into negative territory, respondents said.

“Even after the economy starts to grow again, it is in such a deep hole that the level of real GDP will remain below potential for several years — giving the Fed room to remain accommodative,” says David Berson, senior vice president and chief economist at Nationwide.

Read on for key findings from Bankrate’s Fed poll, which gauged 15 financial and economic experts between June 1-3 on where they see monetary policy and the Fed heading in the years to come.

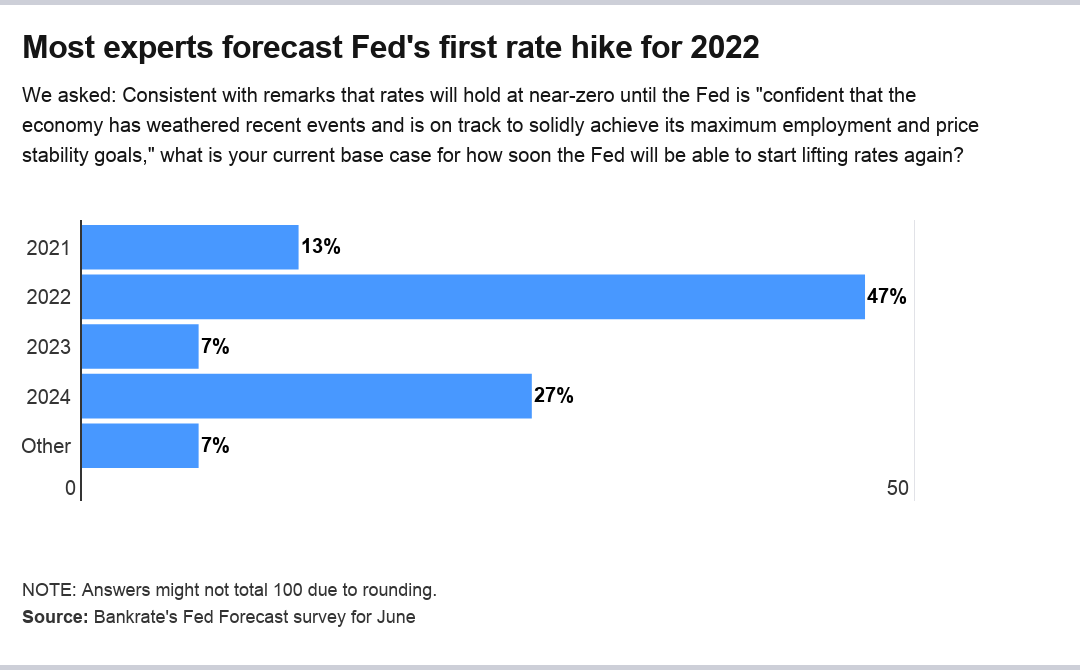

Interest rate outlook: Most economists see no rate hikes until 2022

The biggest cluster of economists estimate that the first rate hike won’t occur until 2022, with about half (or 47 percent) saying the U.S. central bank is unlikely to hike borrowing costs until then, according to the poll. That’s in line with what experts estimated during the April Fed Forecast survey period.

“It’s a very deep hole to dig out of, so it’s highly unlikely to be next year,” says Dan North, chief economist at Euler Hermes. “But given the expectation of a U-shaped rebound, 2022 seems feasible.”

Powell has echoed in multiple statements that the Fed will want to make sure the economy is solidly on the road to recovery while also on track to achieve its dual mandate of maximum employment and 2 percent inflation. With economists estimating that unemployment will remain in the double digits into 2021, according to a separate Bankrate economists’ poll from June, it all suggests that the half-century lows in unemployment experienced before the pandemic aren’t going to return anytime soon.

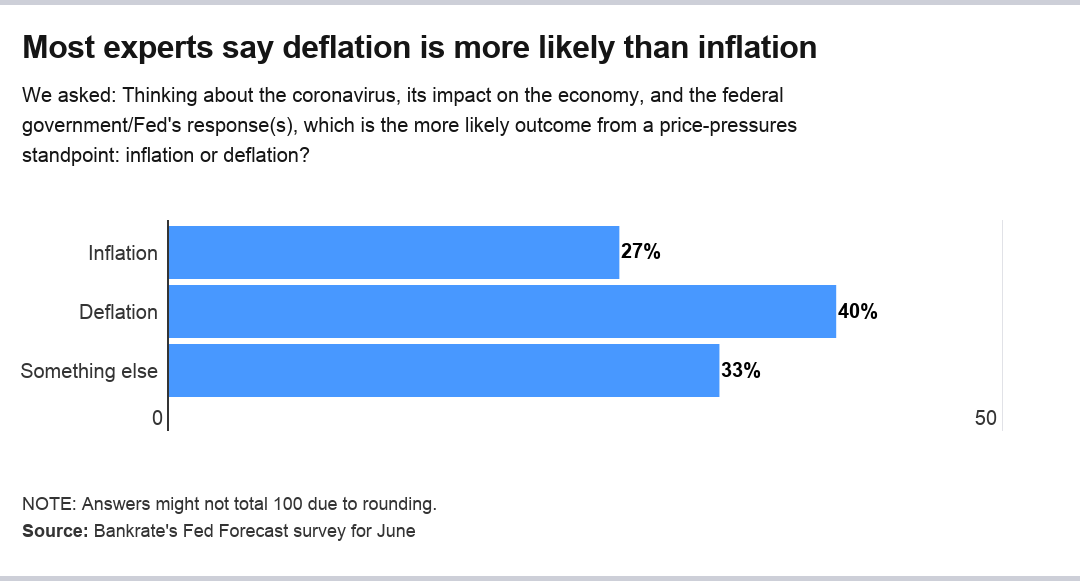

Which is more likely: Inflation or deflation?

But the inflation side of the Fed’s dual mandate has been a bit of a wildcard during the pandemic. As the Fed and Congress flood the markets with monetary and fiscal stimulus, some experts have estimated that price pressures will build down the road. Others, however, have warned that the overall weak economic outlook combined with a decline in payrolls and spending will lead to deflation.

Experts surveyed by Bankrate say that deflation (40 percent) is more likely than inflation (27 percent), though 33 percent say they’re expecting something else. Within their written responses, experts indicated that disinflationary pressures are more likely than outright deflation, while others estimate that short-term deflation will be accompanied by longer-term inflation.

But the Fed might welcome a pick up in prices, given that price pressures have been undershooting the Fed’s target for most of the past decade.

“Textbook theory on the Fed tells us they equally weigh their two mandates of labor markets and price stability. But in reality that is not the case,” says Samantha Azzarello, global market strategist at J.P. Morgan Asset Management. “The Fed has to juggle priorities, and I would say right now the priority is healing the labor market and getting millions of Americans back working. That takes priority even if we started to see a bit of inflation.”

That would, of course, imply that rates are kept lower for longer. Economists who are predicting the Fed won’t be able to raise rates until 2023 or beyond are largely basing those forecasts on history.

“After the 1990 and 2001 recessions, it took about two and a half years from the end of the recession for the Fed to begin raising rates. The Great Recession, on the other hand, was deeper than those previous two, and therefore it took longer — around 6.5 years — for the Fed to start lifting rates,” says Deron McCoy, chief investment officer at Signature Estate and Investment Advisors. “If this recession were to end in Q4, then 2-3 years would take us out to Q1-Q2 of 2023. Considering we’re experiencing a GDP decline that’s much more severe than the Great Recession, perhaps it will take longer.”

The Fed in June is poised to release an update of its economic projections for the first time since December, which will contain its widely watched “dot plot” chart. Those forecasts will offer some clues into when officials are expecting to lift off from zero.

New tools: Expect yield curve control and balance sheet expansion, but not negative rates

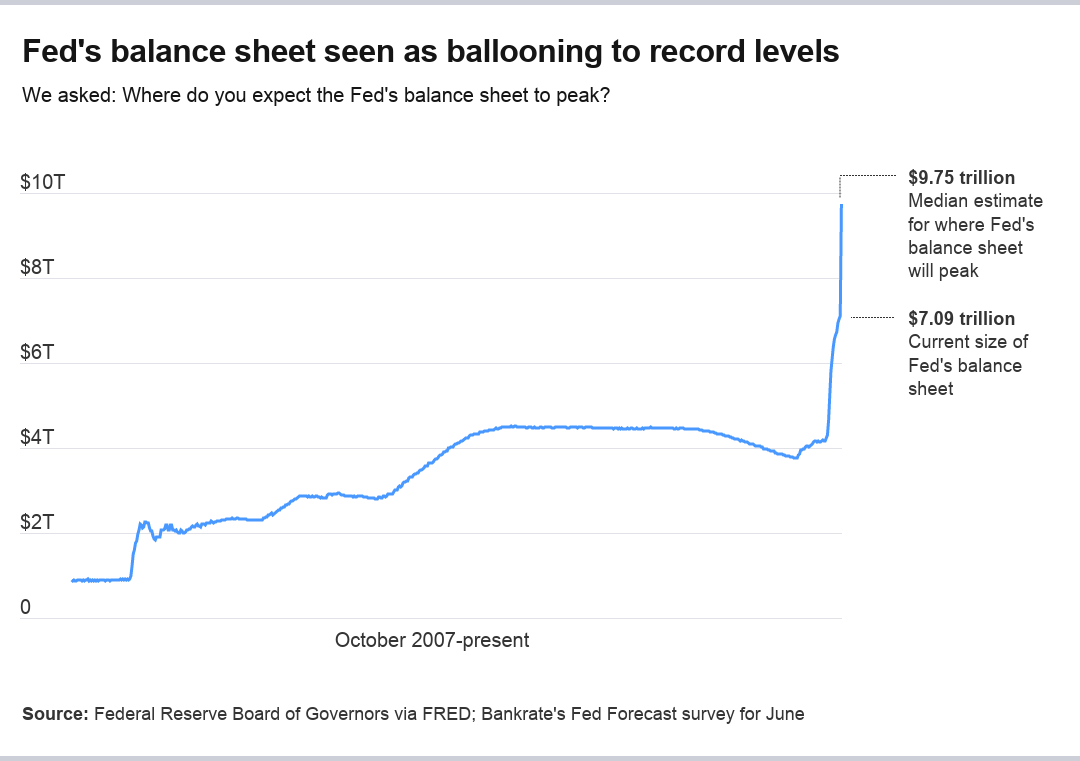

In addition to cutting interest rates to zero, the Fed has pledged to buy as many government bonds as necessary to ease dysfunction in markets while also lending to companies big and small, as well as states and municipalities, through its 11 emergency lending programs.

Those efforts have all caused the balance sheet to balloon to unprecedented levels, surging to above $7 trillion for the first time in the Fed’s history. By comparison, the Fed’s balance sheet ballooned to $4.5 trillion following its emergency responses surrounding the Great Recession of 2007-2009.

But the Fed’s total number of assets and liabilities is bound to grow even larger than where it is now, once all of its emergency lending efforts are said and done, according to Bankrate’s poll. The balance sheet will peak around $9.75 trillion, according to the median forecast among economists.

Why is the balance sheet important? It’s just another tool that Fed officials use to increase the size of banks’ reserves and the money supply. But through history, it’s also been a crucial way of putting even more downward pressure on interest rates.

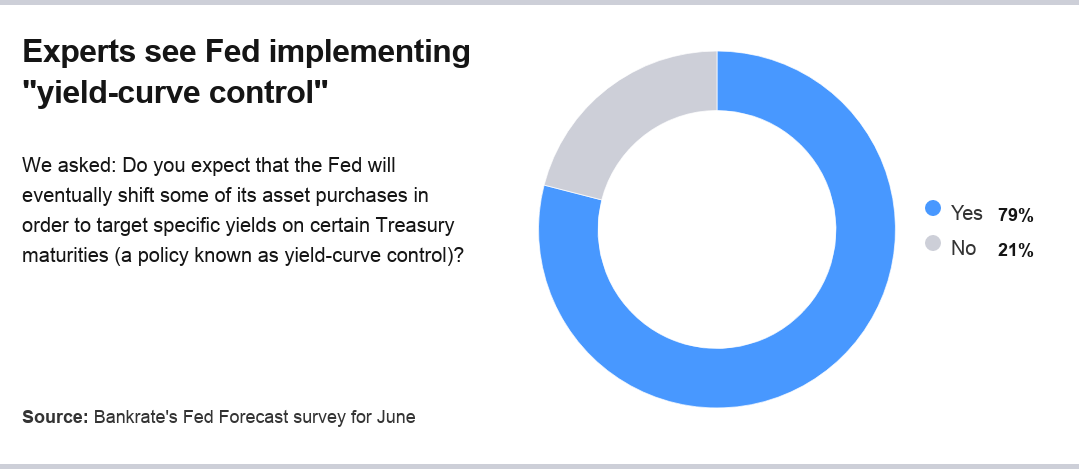

The majority (or 79 percent) of economists expect the Fed to introduce a program commonly known as “yield-curve control” at some point in 2020, which would fulfill that side of the balance sheet’s function.

Similar to quantitative easing (Q.E.), these steps involve the Fed shifting its asset purchases to a broader range of securities to target a certain yield on government bonds all along the curve. Some experts have noted the Fed could do this by capping yields on the 3-year and 5-year Treasurys, or it could also shift to capping yields as far out as the 10-year note, a strategy adopted by the Bank of Japan.

With all those steps in mind, 93 percent of experts are not expecting the Fed to adopt a negative interest rate policy at any time in the future — in line with officials’ comments despite rising bets from investors on Wall Street.

“Powell & Co. seem to be very stern on not rolling out negative interest rates,” says Jamie Sullivan, CFO at Tru Independence. “It would take another very significant economic event or downturn to get the Feds to implement negative interest rates. It’s being viewed as an absolute last-resort measure, given the mixed response and ambiguous implications we’re seeing from other central banks that have rolled them out over the past years or decades.”

One of those outcomes is deflation, according to the survey’s sole financial expert who believes the Fed will cut rates below zero at some point.

“Deflationary pressure will continue to build,” says Robert Phillips, managing member at Spectrum Management Group. “Even at zero interest rates, the real interest rate will be positive with deflation. In order to keep the real rate at manageable levels, the Fed will eventually allow negative rates.”

Grading the Fed’s response: Most economists give high marks

The Fed’s coronavirus playbook has been wide-ranging and a mixture of something borrowed and something new when it comes to monetary policy.

The Fed created its corporate and municipal credit facilities from scratch, while slashing rates to near-zero and kickstarting its commercial paper and money market mutual funds facilities are an extension from its Great Recession response.

Powell & Co. earned top marks from Bankrate’s survey respondents, with 73 percent of experts giving U.S. central bankers an “A” grade for how quickly and swiftly they responded to the current crisis, as well as how well they communicated their actions.

“The Fed’s actions prevented this health and economic crisis from becoming a financial market crisis that would have led to even worse economic outcomes, especially even higher unemployment,” says Steven Friedman, senior economist at MacKay Shields who formerly worked at the New York Fed. “The Fed stepped in very quickly to extend their lender of last resort capability to higher-rated corporations as well as state and local government. Yes, there is some moral hazard involved in these actions, but that cost pales in comparison to the economic hardship that would have resulted from a more conservative set of policy actions.”

The three participants who gave the Fed “B” marks did so because of its slow rollout of the Fed’s Main Street lending programs, as well as other long-standing challenges: communication and moral hazard.

“It was a very aggressive response which investors liked, but it still wasn’t communicated well to the ‘man on the street,’” North says. “It was great to lubricate the financial system and keep credit flowing, but the massive increase in the balance sheet will be impossible to back out of (remember they tried last September and it was a disaster?), and at some point this policy of extraordinarily easy money for an extraordinarily long time will lead to tears.”

What this means for you

Bankrate’s June Fed Forecast underscores that this low-rate world isn’t going anywhere anytime soon. Take advantage of cheap borrowing costs by paying down debt and refinancing your mortgage, if you’re a homeowner.

Meanwhile, if inflation or deflation becomes an issue, that might lead to some challenges for your wallet. Inflation would eat away at your purchasing power, pushing up interest rates along with prices while also diminishing your returns on savings accounts and other fixed-income assets. Deflation, on the other hand, might mean that your paychecks don’t go as far as they used to.

But no one — not even Fed policymakers — knows just how long the economic hardship will last or how painful it will get. Experts say it’s wise to prioritize building your emergency savings, if you haven’t already done so.

“With Fed Chair Powell expressing concerns about the risk of prolonged recession, weak recovery and lasting damage, and all that we are seeing now about the pace of re-opening, it is unlikely that the U.S. economy will be back on its pre-shutdown growth trajectory before 2024,” says Steven Skancke, chief economic adviser at Keel Point and a former Treasury staffer.

Methodology

Bankrate’s June 2020 Federal Reserve Forecast survey of economists and financial experts was conducted from June 1-3 via an online poll. Survey requests were emailed to potential respondents nationwide, and responses were submitted voluntarily via a website. Responding were: Kristina Hooper, chief global market strategist, Invesco; Paul Schatz, president, Heritage Capital; Peter Earle, research fellow, American Institute for Economic Research; Sal Guatieri, director and senior economist, BMO Capital Markets; Deron McCoy, chief investment officer, Signature Estate and Investment Advisers; Samantha Azzarello, global market strategist, JP Morgan Asset Management; Gary Zimmerman, CEO, MaxMyInterest; Steven Skancke, chief economic adviser, Keel Point; David W. Berson, SVP and chief economist, Nationwide; Jamie Sullivan, CFO, Tru Independence; Steven Friedman, senior economist, MacKay Shields; John Ham, CFA, associate advisor, New England Investment & Retirement Group; Robert Phillips, managing member, Spectrum Management Group; and Jay Bryson, acting chief economist, Wells Fargo.

(Featured image by Adobe Stock; Illustration by Bankrate)

Why we ask for feedback Your feedback helps us improve our content and services. It takes less than a minute to complete.

Your responses are anonymous and will only be used for improving our website.

Sarah Foster is a former U.S. economy reporter and analyst for Bankrate. She’s covered the Federal Reserve and U.S. economy since 2018, when she joined the economics news team at Bloomberg News.

You may also like

Fed lowers interest rates with surprising jumbo half-point cut