Taper, explained: How the Fed plans to slow its bond purchases without wrecking the economy

The U.S. economy continues to rebound from the coronavirus pandemic, but that doesn’t mean the Federal Reserve’s crisis response is over. Next up comes another important stage, one that’s bound to have an impact on consumers’ wallets for years to come: Weaning the world’s largest economy off of the extraordinary accommodation that came with the COVID-19 crisis.

The Fed’s two most high-profile ways of stimulating an economy during a severe recession — are cutting interest rates and purchasing government-backed debt. Those moves are intended to keep the economy awash with credit and borrowing costs cheap.

Yet, when the financial system is ready, the Fed will eventually start to raise interest rates and gradually decrease how many bonds it’s buying each month, in a policy known as “taper.”

While consumers might be able to easily infer how hiking interest rates affects their finances, taper’s implications can often be much more complex. Here’s everything you need to know about the next stage of the Fed’s crisis response, including what taper is, how it could work and how it could impact you.

What is taper?

Taper refers to a post-crisis asset purchase plan, where the Fed, at a predetermined pace, starts to slowly and gradually decrease how many assets it’s buying each month (the process of purchasing securities for stimulative purposes is commonly called quantitative easing, or Q.E. for short).

In today’s case, the Fed is currently buying $80 billion worth of Treasury securities and $40 billion of mortgage-backed bonds each month, the largest asset purchase program in Fed history that illustrates the severity of the pandemic-induced recession. The Fed purchases those assets on the open market and then adds it to its balance sheet, which has ballooned to more than $8 trillion since the pandemic.

When the Fed ultimately decides that it’s time to taper those purchases, it won’t have been the first time it’s done so. Following the financial crisis of 2008, the Fed in December 2013 began reducing its mortgage-backed and Treasury security purchases by a cumulative $10 billion each month. The process concluded 10 months later, when those purchases hit zero.

“The precedent is that they dialed back their stimulus at a stated pace, and they adhered to that,” says Greg McBride, CFA, Bankrate chief financial analyst. “And unless circumstances would dictate otherwise, expect something similar this time.”

Taper, however, is not to be confused with selling assets and shrinking the balance sheet. Rather, the Fed is simply gradually reducing over a certain period of time how much it’s buying.

“Even if tapering begins, we still have an incredibly accommodative monetary policy,” says Kristina Hooper, chief global market strategist at Invesco. “The Fed is still going to be buying assets, just at a lower rate than it had in the past. There are certainly reasons why the Fed would be motivated to begin tapering this year, even if there are a few hiccups (in the economy).”

How the Fed could taper following the impact of COVID-19

Assuming that the Fed announces its bond taper in November, records of the Fed’s September meeting show that officials might want to kickstart the process by either mid-November or early December and conclude the process by mid-2022. The way the math works out, that would mean reducing Treasury purchases by $10 billion each month and mortgage-backed securities by $5 billion each month, though they could always adjust the pace depending on how the economy is performing.

Fed officials also say they’d taper both mortgage-backed and Treasury security purchases at the same time.

Why the Fed is about to taper

Officials have been slowly but surely foreshadowing the upcoming bond taper for the past four months.

Fed officials in July first admitted that the economy had shown progress in its rebound from the pandemic, while records of that rate-setting meeting showed that “most” participants could see a bond-buying slowdown beginning at some point this year.

Officials then followed that up at their November meeting by saying that adjusting their monthly asset purchases may “soon” be warranted.

The Fed has said that it’d like to see the recovery make “substantial further progress” toward its objectives of stable prices and maximum employment before tinkering with its bond-buying program.

On the one hand, inflation has soared, with the Fed’s preferred measure of inflation showing that prices are increasing at their fastest pace since 1991.

The job market is also on track for improvement, though scars remain. Nearly 5 million positions are still missing from the economy, and about 3.1 million workers dropped out of the labor force. Many of those are likely retirements, as well as workers dealing with child care restraints and virus concerns.

At the same time, Powell has indicated confidence that the labor market will get back on track. One such indication: Employers in August had a near record number of job openings (10.4 million), suggesting that the imbalance is coming from a dwindling labor supply, rather than economic uncertainty holding back hiring.

“If you look at the number of job openings compared to the number of unemployed, we’re clearly on a path to a very strong labor market with high participation, low unemployment, high employment, wages moving up across the spectrum,” Powell said in July.

How tapering could impact you

Tapering assets isn’t free from risk. Powell said in 2019 that he’s still scarred from a market sell-off in June 2013, known today as the “taper tantrum.” Then-Fed Chairman Ben Bernanke suggested the economy would soon be strong enough for the Fed to start slowing down its monthly asset purchases, which resulted in a bond and stock market sell off, with equity prices failing and yields soaring.

While experts say the Fed has certainly been more calculated in its communications surrounding taper this time around, consumers might want to brace for volatility, at least in the stock market. Keep a long-term mindset and avoid making any knee-jerk reactions to downdrafts in the market. Better yet, see any market downdraft as a buying opportunity, McBride says.

“In the long run, if the economy is getting better, so too are corporate profits, and that’s ultimately what drives stock prices,” McBride says. “If they (Fed officials) continue to check those boxes, they won’t have to worry about a redo of the taper tantrum — at least in the bond market.”

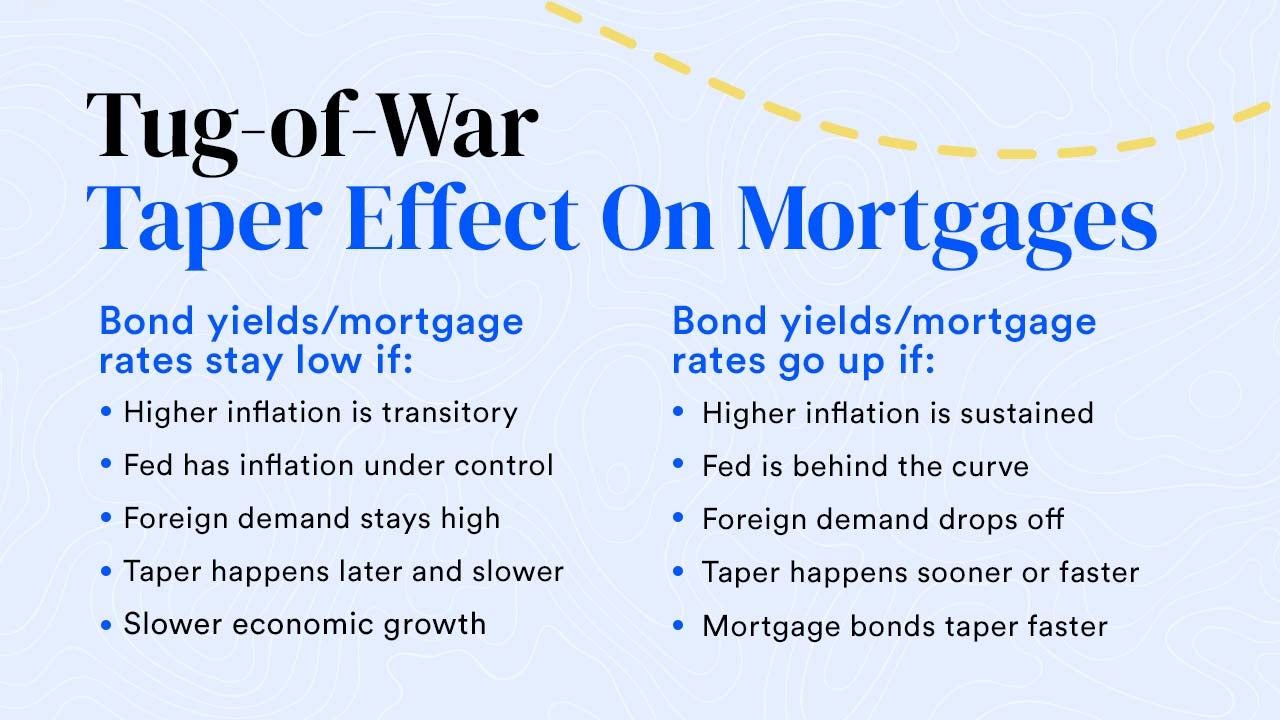

How the Fed’s eventual taper could impact mortgage rates is also up in the air. Typically, yields would rise once the biggest buyer in the marketplace steps away, which could cause mortgage and refinance rates to also go up. But investors also take into account their expectations for inflation when buying Treasurys.

Mortgage rates already started to rise in the weeks leading up to the Fed meeting, with experts attributing that to the Fed’s likely taper at its November meeting. Yet, the 10-year U.S. Treasury yield at the end of October sank by the most since the end of July as investors looked to a likelihood of subdued economic growth and higher inflation.

“The Fed tapering could also be perceived by the market as a more hawkish stance on inflation,” McBride says. “You could actually see long-term yields hover near current lows or move even lower.”

The Fed has said that taper doesn’t mean rate hikes are around the corner, though higher inflation and a booming job market could force officials’ hands. Policymakers are already moving up their rate projections, with the Fed’s September projections suggesting a rate hike could occur as soon as 2022.

Mortgage rates have fallen to historic lows since the start of the pandemic, yet a Bankrate survey from July found that 74 percent of homeowners with a mortgage have not yet refinanced. Would-be refinancers haven’t yet missed their chance, though the refinance window could narrow at a moment’s notice.

“Time is always of the essence because rates can move suddenly, and if they move suddenly, your potential savings can diminish quickly,” McBride says. “I don’t know that the prospect of tapering by itself means people should refinance quickly as much as just the volatile nature of rates. The tremendous savings opportunity that currently exists should get people to refinance as soon as they can.”

Learn more:

- How the Federal Reserve affects mortgage rates

- Programs and tactics to help you afford to buy a home

- Here’s what does (and doesn’t) drive mortgage rates

Why we ask for feedback Your feedback helps us improve our content and services. It takes less than a minute to complete.

Your responses are anonymous and will only be used for improving our website.

Sarah Foster is a former U.S. economy reporter and analyst for Bankrate. She’s covered the Federal Reserve and U.S. economy since 2018, when she joined the economics news team at Bloomberg News.

You may also like

Fed holds interest rates steady, resisting pressure from Trump